Mind the Gap - women in the spotlight!

Mind the Gap - women in the spotlight!

The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2023, in other words this year’s Nobel Prize in Economics, awarded to Claudia Goldin has brought the gender gap in the labour market into the spotlight. Rosa Abraham and Surbhi Kesar have a good overview of her contribution, also pointing out where the learnings fall short for India.

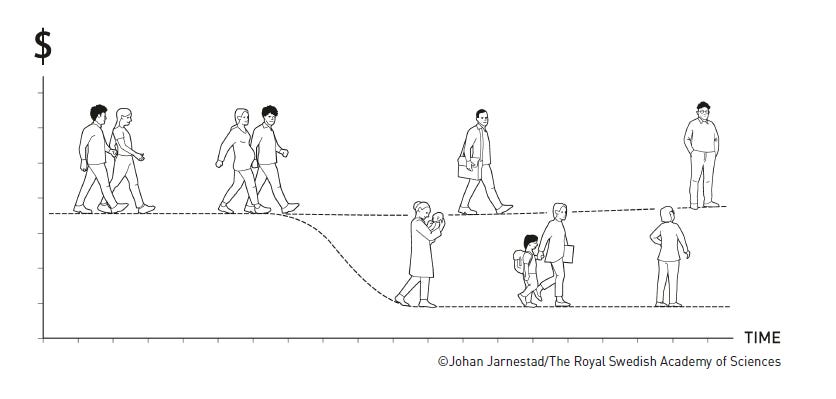

Goldin’s work has implications for the financial inclusion mission in India where the gender gap still needs to be closed. A key insight from her research is that there is a significant earnings gap between men and women in the same occupation, and this gap begins with parenthood. The illustration above makes the path of the earnings gap within the same occupation clear. This is a home truth for us in India, where family responsibilities take precedence for women over paid work outside the home.

Those of us in the financial inclusion space have also seen this glaring gap amongst business correspondents. In a recent study on the pivotal role played by Bank Sakhis in digital financial inclusion for the states of Bihar and Odisha, Rohanshi Vaid and Ammu George have written on the challenges faced by these women in the field, and the fact that they earn less than their male counterparts. Previous research by CGAP on the Bank Sakhi programme in Bihar showed that Bank Sakhis are more effective at enabling financial inclusion of hard-to-reach rural and vulnerable customers compared to male business correspondents, and yet, their business performance was worse than their male counterparts.

Unlike the US, we have a long way to go to fix gender parity in jobs as well. With the Women’s Reservation Bill passed by our Parliament in September, Tamal Bandopadhyay took a quick overview of where India stands on the gender gap in employment, and zoomed into the low score of women in the banking sector. Even at the RBI, less than a quarter of the staff are women, and the proportion at the top levels of leadership is quite insignificant. The fact is that the banking sector on a whole has a below-average presence of women on the rolls. While this has an impact on the design of suitable policies and products, this would even affect the comfort level of women customers at the branches, creating an additional barrier for inclusion.

The point that finance has to be gender intentional, and not gender-neutral comes through very clearly in Joanna Ledgerwood’s excellent wrap of conversations at the Responsible Finance Forum - a must read for pointers towards closing the gender gap in financial inclusion. Chetna Gala Sinha’s comment, “Women don’t need to be educated, bankers do!” comes from her experiences with women customers and bank managers and rings true across studies.

While bank deposits by women are growing significantly, they are still not part of banking in proportion to their numbers, as Sunaina Kumar points out. On the credit side, a deep divide continues. An interesting research by Microsave in partnership with SEWA into the journey of women-owned MSMEs in credit access brought out this point that as women found the process of seeking loans from mainstream banks quite inconvenient and time-consuming, many dropped out of the process. Interestingly, the study also showed that women credit seekers are not a homogenous group and identified five categories of women owning MSMEs on the demand side. The research also highlighted the positive role played by bridge institutions like SEWA, JEEViKA, Utkarsh Welfare Foundation and others.

Somehow, when it comes to empowerment of women, there is still a tendency to lump all models in one basket – and the conflation, even by the RBI, of two women-centric models, that is Microfinance institutions and Self-help groups, has been called out by Indradeep Ghosh and Anand Raman. What is the difference? “One begins with a moral commitment and overlays it with an economic calculation. The other begins with an economic calculation and overlays it with a moral commitment. This difference makes for different ‘cultures’ and operating dynamics.” As they rightly say, recognizing the critical difference between the two has implications for regulatory and state support.

Finally, even as the financial services industry and policy makers grapple with closing the gender gap in financial inclusion, we need to keep in mind that women are not a homogenous group. And this piece by Rani Deshpande reinforces the need for further segmentation, by focusing on young women in the critical age group 15-24 years- one financial inclusion intervention suggested is combining financial education with a financial service/product, perhaps related to health, and given through female mentors in the community. Such intervention at a young age can make a transformational change not just for women individually, but for the society at large.

***

Do follow our Indicus Centre for Financial Inclusion page on Linkedin to continue the conversation. Read on here for more of the latest news and views on financial inclusion in India, thanks!

Anil Padmanabhan analyses whether Open Credit Enablement Network (OCEN) will be a gamechanger for MSMEs.

Deepsekhar Choudhury writes for Moneycontrol on the Open Network for Digital Commerce (ONDC) scaling new highs in orders.

Gaurav Noronha writes for The Ken on the nod by RBI for the Slice-North East Small Finance Bank merger that shows that the regulator is open to using fintechs to rescue troubled banks.

Vishwanath Nair writes for BQPrime to explain why the Reserve Bank of India gave a no-objection certificate for a merger between fintech unicorn Slice and North East Small Finance Bank.

Pratyaksh Shrivastava, Gaon Connection brings together reports from the ground on the foot soldiers of banking in rural India – the army of business correspondents.

Sophie Sirtaine,CGAP writes a comprehensive and insightful piece on the future of financial inclusion.

Swati Mehta, CFI Accion, reports on the results of a study by CFI and WFP that examined how cash transfers to women on behalf of their households can reduce risk factors associated with intimate partner violence.

Anita Suri writes on how women are unlocking financial inclusion in rural India, with the collective efforts of fintech, government and financial institutions.

Caroline Pulver, Joep Roest and Myra Valenzuela, CGAP begin a three part series on how government payments programme can be linked with comprehensive climate risk management policies and include long-term adaptation in their design.

Pramiti Lonkar, Shweta Menon and Akshat Pathak, MicroSave, write on NPCI’s innovative offline payment solution, UPI 123Pay, and its immense potential to bring digital payment convenience to the underserved segment.

Mitali and Shweta Menon, MicroSave, write about the crucial role ONDC could play to unlock lending opportunities for MSMEs and improve their access to online marketplaces.

Elizabeth Kiamba, CGAP reports on the insights from a study that showed how gig platforms can help workers towards regular savings from irregular income.

Manali Jain, Shweta Menon, Akshat Pathak and Pramiti Lonkar, MicroSave, have a two-part series highlighting the evolutionary and revolutionary initiatives in India that are currently driving the growth of digital payments.

Sonal Jaitly, Poulomi Ghosh, Sheetal Prasad and Mann Soni, MicroSave, released results from a study—Mentorship for Women Entrepreneurs—A Highway to Growth,” that attempted to understand women entrepreneurs’ awareness, access, experience, and perceptions of the value derived from mentorship.

Deepak Maheshwari writes an insightful post on a holistic policy framework for digital inclusion.

Urvashi Mishra writes for Fortune India on the insights from a report, "AI revolutionises inclusion and profitability for financial services’, brought out by Google and McKinsey & Company.

Reserve Bank of India announced the Financial Inclusion Index value for the year ending March 2023 : "The value of FI Index for March 2023 stands at 60.1 vis-à-vis 56.4 in March 2022, with growth witnessed across all sub-indices.